In 2026, many UAE businesses are facing compliance issues not because of tax evasion, but due to missed VAT deadlines, incorrect returns, or delayed error corrections.

With stricter enforcement, faster data matching, and increased scrutiny on VAT submissions, even a small mistake can lead to penalty escalation, rejected returns, or compliance flags. This risk is especially high for businesses that file VAT returns without a clear compliance calendar or fail to correct errors through VAT voluntary disclosure.

With late‑filing fines, compounding late‑payment charges, and error‑based penalties that can reach up to 300% of unpaid VAT, leaving mistakes uncorrected has become significantly more expensive in 2026.

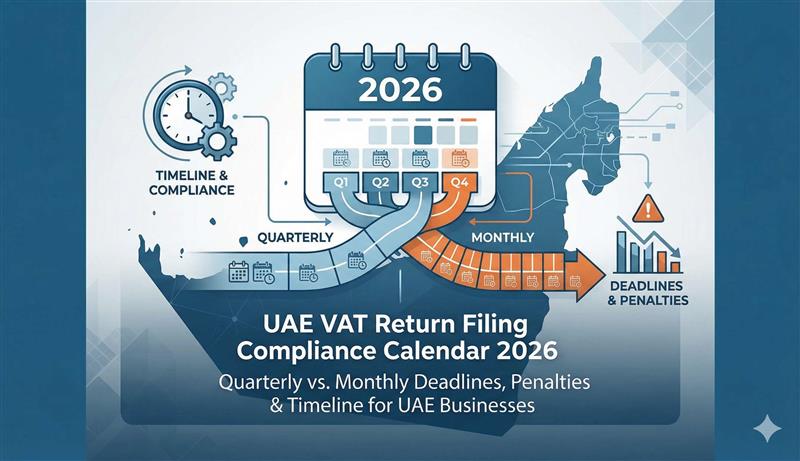

Understanding VAT return filing timelines, knowing whether you fall under quarterly or monthly filing, and acting promptly when errors are discovered is essential to avoid unnecessary penalties in 2026.

This guide explains how VAT return filing works in the UAE, key deadlines, penalties, and how businesses can restore compliance when issues arise.

All VAT-registered businesses in the UAE are required to file VAT returns as per their assigned tax period.

VAT return filing is regulated by the Federal Tax Authority, and applies to:

Failure to file accurately and on time exposes businesses to financial penalties and audit risk.

Most VAT-registered businesses in the UAE file quarterly VAT returns.

Some businesses are assigned monthly VAT filing due to their transaction volume or risk profile.

Your filing frequency is assigned by the FTA and cannot be changed without approval.

As a general guideline, businesses with annual taxable supplies below AED 150 million are typically assigned quarterly returns, while those at or above AED 150 million are often placed on monthly filing, subject to FTA discretion.

VAT returns must be:

Both the VAT return and the VAT payment must reach the FTA by the deadline, and the exact due date for each tax period is shown in your EmaraTax account, which should be checked regularly.

Missing the deadline by even one day can trigger penalties.

The FTA may set different due dates in specific cases, so the EmaraTax dashboard should always be treated as the final reference for deadlines.Businesses should maintain a VAT return filing compliance calendar to avoid deadline slippage.

Many businesses only identify VAT issues after filing, internal review, or FTA notification.

Common issues include:

Ignoring discovered errors increases penalty exposure.

When a VAT error is identified after submission, businesses must use VAT voluntary disclosure.

VAT voluntary disclosure allows businesses to correct errors transparently and reduce compliance risk.

Under current rules, VAT errors must generally be disclosed within 20 business days of being discovered, and voluntary disclosure via Form 211 attracts fixed and percentage‑based penalties that are lower than those applied when the FTA finds errors first.

Delaying disclosure often results in higher penalties during audits.

VAT penalties in 2026 are increasingly enforcement-driven.

Potential penalties include:

For repeated non-compliance, businesses may face enhanced scrutiny or audit selection.

Poor VAT compliance impacts more than tax records.

Risks include:

For businesses seeking compliance restoration, timely correction is critical.

ASC Global supports UAE businesses with end-to-end VAT compliance, including high-risk and corrective scenarios.

Our services include:

We help businesses restore compliance, reduce penalties, and prevent repeat issues.

Q1. Is VAT return filing mandatory even if there is no activity?

A1. Yes. Nil returns must still be filed within the deadline.

Q2. What happens if my VAT return is rejected by the FTA?

A2. Rejected returns must be corrected and resubmitted promptly, and if the rejection relates to errors in a previously filed period, a voluntary disclosure (Form 211) may be required to correct the VAT position formally.

Q3. Can VAT voluntary disclosure reduce penalties?

A3. In many cases, timely disclosure helps mitigate penalty severity.

Q4. Does quarterly filing mean lower compliance risk?

A4. No. Accuracy and timeliness matter regardless of filing frequency.

Q5. How far back can the FTA audit VAT returns?

A5. The FTA can generally audit VAT periods going back several years, and businesses must retain VAT records for at least 5 years from the end of each tax period, with longer retention for certain assets such as real estate.

In 2026, VAT return filing in the UAE is no longer a routine task. With tighter controls, faster enforcement, and higher penalties, businesses must treat VAT compliance as a core financial responsibility.

Whether you are managing quarterly filings, monthly submissions, or correcting past errors through voluntary disclosure, timely action is the key to avoiding penalties and restoring compliance.

Professional oversight ensures VAT obligations are met accurately, consistently, and defensibly.

📞 Call: +971503287722

💬 WhatsApp: https://wa.me/971503287722

🌐 Visit: www.ascglobal.ae

📩 Email: info@ascglobal.ae

ASC Global UAE — your trusted partner for VAT return filing, deadline management, penalty mitigation, and FTA audit-ready tax compliance.

VAT Advisory

VAT Advisory

➤ Introduction – Why FTA Bookkeeping Requirements UAE Matter in 20252025 marks a turning point for tax compliance in the...

Read MoreOffice 04 - 1803, 18th floor, One by Omniyat Business bay, Dubai

302-18 Edgecliff Golfway, North York, Toronto, Ontario M3C 3A3

Via F.lli Gabba 3, 20121 – Milan, Italy

RM2106, Huishangsha Edifice, No.37, Baoshi West RD, Shiyan Town, Bao’an District, Shenzhen - 518108, China

C-100, Sector 2, Noida (UP), Delhi NCR, India 201301

One Raffles Place, Tower 1, 27-03 Singapore - 048616

Merger & Acquisition

Merger & Acquisition Due Diligence

Due Diligence

Business Advisory

Business Advisory Business Setup & PRO

Business Setup & PRO Corporate Tax Advisory

Corporate Tax Advisory Accounting & Assurance

Accounting & Assurance Risk Advisory

Risk Advisory Tech & Cyber Security

Tech & Cyber Security VAT Advisory

VAT Advisory